Utilization of Input Tax Credit under GST Rule 88A, Section 49A and 49B

GST

Vaishali Patel

6/28/20253 min read

Rule for utilization of input tax credit – section 49(A) and rule of order of utilisation of input tax credit – 49(B) under CGST Act 2018 were introduced by CBIC in February 2019. Thus laying new criteria for a registered person to discharge his/her GST liability. However, following the insertion of the amendment, many businesses raised a concern regarding the blockage and accumulation of credit under the CGST and SGST category. And such accumulation could further lead to cash flow issues wherein the suppliers would be required to pay the tax in cash even when they have the unutilised credit available in their electronic credit ledger.

Thus, in an attempt to ease the cash flow concern of trade industry in India, the government has notified relaxations in ITC set-off mechanism vide GST Notification number 16/2019 – Central Tax dated 29th March 2019 with the insertion of Rule 88A.

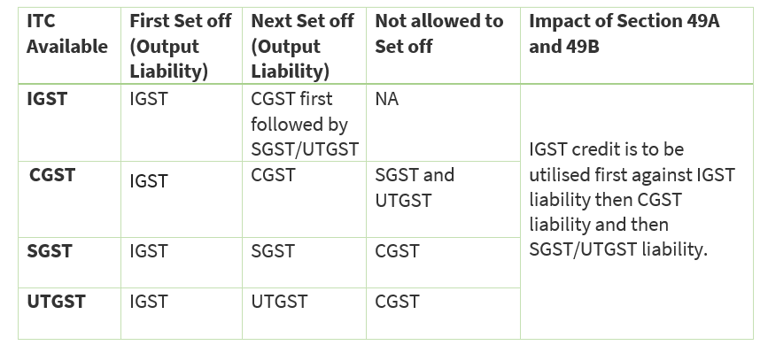

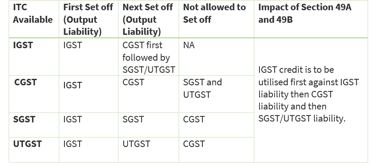

Utilization of ITC before April 1, 2019

(After the introduction of Section 49A and 49B)

Effective February 1, 2019, Section 49A and 49B were introduced in the CGST Amendment Act 2018.

1. Section 49A: Utilisation of input tax credit

Notwithstanding anything contained in section 49, the input tax credit on account of central tax, State tax or Union territory tax shall be utilised towards payment of integrated tax, central tax, State tax or Union territory tax, as the case may be, only after the input tax credit available on account of integrated tax has first been utilised fully towards such payment.

2. Section 49B: Order of utilisation of input tax credit

Notwithstanding anything contained in this Chapter and subject to the provisions of clause (e) and clause (f) of sub-section (5) of section 49, the Government may, on the recommendations of the Council, prescribe the order and manner of utilisation of the input tax credit on account of integrated tax, central tax, State tax or Union territory tax, as the case may be, towards payment of any such tax.”

Thus, for example, if after setting of IGST Liability, IGST ITC credit available is Rs. 12,000 and CGST liability is Rs. 12,000 and SGST Liability is Rs. 2,000, then IGST credit will be utilised against CGST liability of Rs. 12,000. Thus balance SGST liability will be Rs. 2,000.

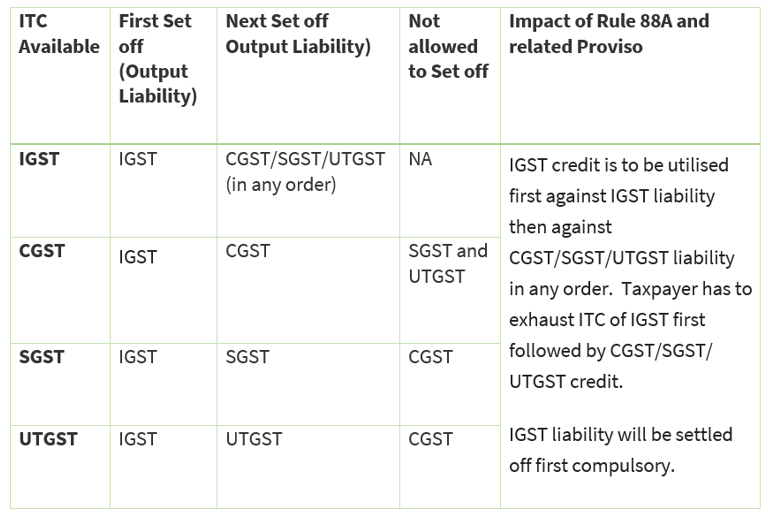

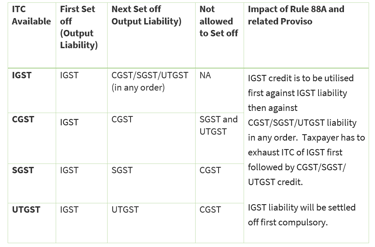

Utilization of ITC After April 1, 2019

Correcting an anomaly regarding input tax credit utilisation under Section 49A of the Central Goods and Services Tax (Amendment) Act, 2018, Rule 88A has been inserted (Notification Number 16/2019 – Central Tax dated 29th March 2019) in the CGST Amendment Act 2018.

Rule 88A: Order of utilisation of Input Tax Credit

Input tax credit on account of integrated tax shall first be utilised towards payment of integrated tax, provided that the input tax credit on account of central tax, State tax or Union territory tax shall be utilised towards payment of integrated tax, central tax, State tax or Union territory tax, as the case may be, only after the input tax credit available on account of integrated tax has first been utilised fully”.

Thus, for example, if after setting of IGST Liability, IGST ITC credit available is Rs. 12,000 and CGST liability is Rs. 12,000 and SGST Liability is Rs. 2,000, then IGST credit can be utilised against the SGST liability of Rs. 2,000 and CGST Liability of Rs. 10,000. Thus balance CGST liability will be 2000.

Key Notes:

· ITC of IGST should be utilised in full before utilising any other credit.

· Taxpayers should note that Utilisation of IGST ITC shall be allowed against any other tax liability only when IGST liability has been fully paid first.

· With the introduction of this rule, the taxpayer after adjusting the IGST liability, can adjust remaining IGST ITC with CGST/SGST/UTGST liability as per their discretion.