Understanding the Supply ‘to & from’ SEZ in GST

This article highlights the treatment of Sales and Purchases with SEZ as per the provisions made under the new GST Returns.

GST

Vaishali Patel

6/28/20252 min read

There are certain geographical areas wherein liberal economic laws are imposed. These areas are called as Special Economic Zone (SEZ). In order to facilitate the supply of goods and services to and from SEZ, separate provision has been made under the GST regime.

This article highlights the treatment of Sales and Purchases with SEZ as per the provisions made under the new GST Returns.

Supply to SEZ unit from a Regular Taxpayer

Sale to SEZ is classified in two ways, SEZ with payment of duty and SEZ without payment of duty.

Supply to SEZ with payment of duty:

Ideally, SEZ units/developers do not have any GST liabilities, however, in some scenarios, they may have to pay GST against an invoice(inclusive of GST) issued by the regular taxpayer. Under such cases, the treatment of GST charged varies case to case. In some cases, the GST amount is collected from SEZ unit/developer and then SEZ takes a refund of such amount from GSTN. In others, GST amount is not collected from SEZ unit/developer instead the regular taxpayers pay GST and then claim refund of the same.

In New GST returns, GSTN has introduced a new way to auto-populate the refund form, with the addition of a new field “Whether Supplier wants to claim refund”. Depending upon the answer selected by a supplier (Regular Taxpayer) i.e. ‘Yes’ or ‘No’ in the given field while uploading the invoice in Table 3E of ANX-1, the invoice will be auto-populated in Table 3A of ANX-2 of the recipient (SEZ Taxpayer).

Supply to SEZ without payment of duty:

Conversely, if your supplier does not collect tax, in such scenarios, such goods/services are termed as SEZ without payment of duty. For goods/services that are sold without payment of duty, the Regular Taxpayer can show this amount in Table 3F of ANX-1 and the same will be auto-populated in Table 3A of ANX-2 of SEZ.

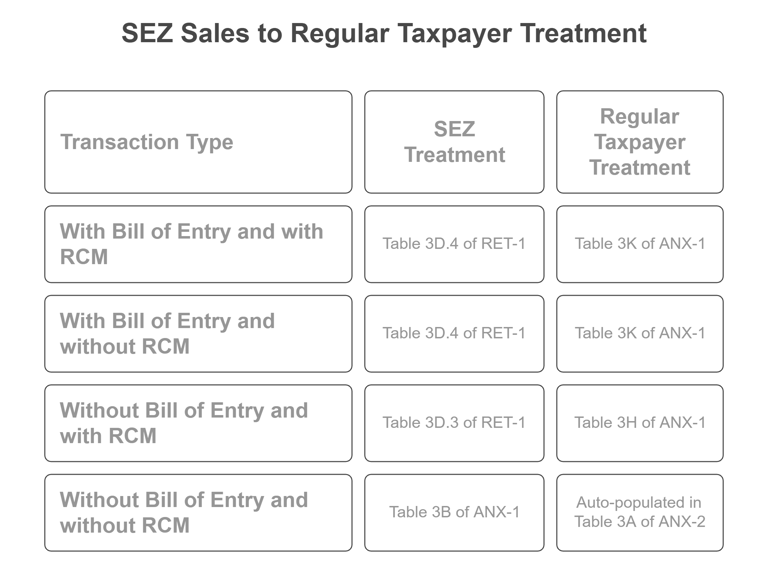

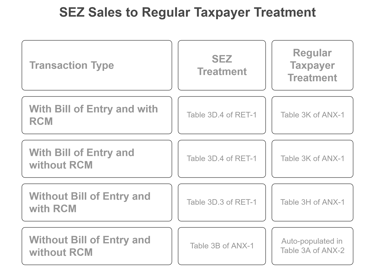

Supply from SEZ unit to a Regular Taxpayer:

Treatment of sales by SEZ is quite different from sales to SEZ. Under GST, an SEZ unit can sell their goods and service with or without the cover of Bill of Entry, which, like any other purchase, can be subject to Reverse Charge Mechanism (RCM).

Sale from SEZ with Bill of Entry

In cases wherein goods are supplied with Bill of Entry, such transaction shall bear no liabilities for the SEZ unit, however, for the buyer (Regular Taxpayer) it will be treated as imports from SEZ.

Sale from SEZ without Bill of Entry

In cases wherein the goods and services are sold without Bill of Entry, then such transaction shall be treated as normal sales and purchase for SEZ and Regular Taxpayer, respectively

P.S: Services are always supplied without Bill of Entry, hence they are treated as normal sales.

Following table depicts the way in which sales by SEZ to a Regular Taxpayer will be treated in new forms: