Section 24 - Tax Deductions From House Property Income

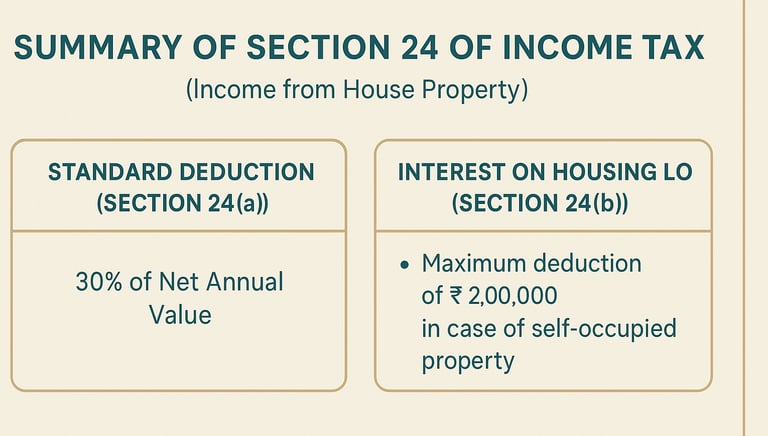

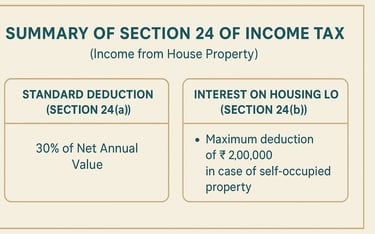

Section 24 of the Income Tax Act provides deductions for income from house property. It allows a standard deduction of 30% of the Net Annual Value and a deduction for interest on housing loans. The interest deduction is capped at ₹2,00,000 per annum for self-occupied properties, while there is no limit for let-out properties.

DEDUCTION

Kashish Raut

5/7/20258 min read

Section 24 - Tax Deductions From House Property Income

Buying a home is one of the most common long-term investment goals for most of the Indians. And once you have bought a home, a great chunk of your income goes towards home loan EMI. Considering this fact, the government has given plenty of tax benefits under Section 24 of the Income Tax Act for the income arising from the house property.

Budget 2025 Update

Previously, the annual value of up to two self-occupied properties was deemed to be nil if the owner is unable to occupy the property due to employment, business, or professional commitments at a different location. It is now proposed that the annual value of up to two house two house properties shall be nil if the owner occupies the house for his own residence or cannot occupy it for any reason.

Income from House Property

The following income will be taxable under the head ‘Income from House Property’ of the Income-tax Act, 1961.

· Rental Income earned on a let-out property

· Annual value of a property which is ‘deemed’ to be let out for income tax purposes (excess properties will be considered as let out properties when you own more than two house property)

The annual value of a self-occupied property is zero or can even be negative if the interest on a home loan is claimed as a deduction. You must be wondering, what is the annual value of a property? The annual value of a property is the expected rental income if the property is rented out.

So, from above point 2, you should deduce that if you have more than two house properties, then excess house properties shall be treated as deemed to be let out property and the annual value of such properties will be included in your taxable income.

You must be asking, what if I do not let out those excess properties? No, that’s not the case whether you let it out or not. The point is government does not allow you to keep more than 2 house properties as self-occupied, so even if you don’t let out the excess house properties, it will be considered as deemed to be let out property.

If the property is let out, the rent received is your Gross Annual Value (GAV). For a deemed to be let-out property, the reasonable rent of a similar place is your Gross Annual Value.

Deductions Under House Property

· Municipal tax – Municipal taxes are the annual amount paid to the municipal corporation of that area. Municipal taxes are to be deducted from the Gross Annual value to derive the Net annual value of the house property. Deduction of municipal tax is allowed only if it has been borne by the owner and paid during that financial year. The amount derived after deducting municipal taxes from GAV is termed as Net Annual Value (NAV).

· Standard Deduction – Standard Deduction is allowed 30% of the NAV calculated above. This 30% deduction is allowed even when your actual expenditure on the property is higher or lower. Therefore, this deduction is irrespective of the actual expenditure you may have incurred on insurance, repairs, electricity, water supply etc. For a self-occupied house property, since the Annual Value is Nil, the standard deduction is also zero on such a property.

· Deduction of Interest on Home Loan for the property –House Property owners can claim a deduction of up to Rs.2 lakh on their home loan interest if the owner or his family reside in the house property. The same treatment applies when the house is vacant. If you have rented out the property, the entire interest on the home loan is allowed as a deduction.

Your deduction on interest is limited to Rs.30,000 if you fail to meet any of the conditions given below:

· The home loan must be for the purchase and construction of a property;

· The loan must be taken on or after 1 April 1999;

· The purchase or construction must be completed within 5 years from the end of the financial year in which the loan was taken

Further, if you have availed the loan for a residential house property during the period between 01-04-2016 to 31-03-2017, you can claim up to Rs.50,000 under Section 80EE over & above the above limit provided under Section 24.

Similarly, if you have borrowed a loan during the period between 01-04-2019 to 01-04-2022, you can claim up to Rs.1,50,000 under Section 80EEA over & above the above-provided ceiling limit of Rs.2,00,000.

Further, Section 80C allows a deduction if you have made any principal repayment of a loan for your house property, including a payment of stamp duty, and registration charge.

Note: Under the New tax regime, no deduction is allowed in respect of interest on loans borrowed for self-occupied property, whereas deduction is allowed with no ceiling limit for interest on loans borrowed for let-out property irrespective of the tax regime you choose.

Under the old tax regime, the deduction under Section 80 series would be allowed for self-occupied properties, as stated above.

Who Can Claim Deductions Under Section 24?

Individuals owning a residential property that generates rental income or is self-occupied are eligible to claim deductions under Section 24.

Types of deductions:

· Standard deduction: A flat 30% deduction is allowed on the gross annual value of the let-out property, regardless of any actual expenses incurred. This makes it hassle-free and convenient.

· Interest on home loan: If you have taken a loan for the acquisition, construction, or repair of the property, you can claim the interest paid on the loan up to certain limits specified as a deduction.

Calculating the Gross Annual Value:

The gross annual value is the fair rental income the property could fetch if rented out in its current condition. It can be calculated as:

· Actual rent received: If the property is rented out, the actual rent received is considered the gross annual value.

· Municipal valuation: If the property is self-occupied or deemed to be let out, the municipal valuation can be used as a proxy for the gross annual value.

To know more about home loan tax benefits ToTo know more about home loan tax benefits

Read the article: claim HRA Deduction & Home Loan Interest

Pre Construction Interest

When you have taken a loan for the purchase or construction of a house property, you can claim a deduction on pre-construction interest. Pre-construction interest is the interest incurred during the construction phase of the house property. The interest incurred during the construction phase is not allowed as a deduction in those years but it is accumulated and allowed as a deduction in 5 equal instalments from the year in which construction is completed.

However, this is not allowed in the case of a loan for repairs or reconstruction.

The total amount of pre-construction interest and interest on a housing loan that can be claimed in a year in case of a self-occupied property should not exceed Rs 2 lakh in any case. The deduction for this interest is allowed in 5 equal instalments starting from the year in which the house is purchased or the construction is completed.

For example, if the construction of your property was completed in FY 2022-23 on 25 June 2022, you can claim 1/5th of the interest paid up until 31 March 2022 when you file your return from FY 2023-24 to FY 2027-28.

Conditions for Claiming Interest on Home Loan

You need to meet all the below 3 conditions to claim this deduction

· The loan has been taken after 1st April 1999 for purchase or construction

· The acquisition or construction is completed within 5 years from the end of the financial year in which the loan was taken

· There is an interest certificate available for the interest payable on the loan. Note that your interest deduction may be limited to Rs 30,000 if any one of these conditions is met –

· The loan is borrowed before 1st April 1999 for purchase, construction, repairs or reconstruction of house property or

· The loan is borrowed on or after 1st April 1999 for repairs or reconstruction of house property or

· The acquisition or construction is not completed within 5 years from the end of the financial year in which the loan was taken

Computation of Income Under House Property

Say, a person repays a housing loan of Rs 4 lakh annually out of which Rs 2 lakh is the interest component. He has also incurred a pre-construction interest of Rs 3 lakh. He is earning Rs 7,000 monthly from a let-out property and also pays municipal taxes of Rs 3,000 for the house. Let’s calculate his Income from house property in both the scenarios:

(1) The property is self-occupied property, or (2) The property is rented out

🏠 Self-Occupied Property

Gross Annual Value (GAV): ₹0

For self-occupied properties, the GAV is considered nil as there's no rental income.Less: Municipal Taxes Paid: Not Applicable

Since GAV is nil, municipal taxes aren't deducted.Net Annual Value (NAV): ₹0

(GAV - Municipal Taxes)Less: Standard Deduction (30% of NAV): Not Applicable

30% of ₹0 is ₹0.Less: Interest on Housing Loan: ₹200,000

Deduction under Section 24(b) is allowed up to ₹2,00,000 for self-occupied properties.Less: Pre-construction Interest (1/5th of ₹3,00,000): ₹60,000

Pre-construction interest is distributed equally over five years.Total Deductible Interest: ₹260,000

However, for self-occupied properties, the maximum deduction allowed is ₹2,00,000.Income from House Property: ₹(200,000)

This results in a loss of ₹2,00,000, which can be adjusted against other income heads as per tax laws.

🏢 Let-Out Property

Gross Annual Value (GAV): ₹84,000

Assuming monthly rent of ₹7,000, annual rent becomes ₹7,000 × 12 = ₹84,000.Less: Municipal Taxes Paid: ₹3,000

Municipal taxes paid during the year are deductible.Net Annual Value (NAV): ₹81,000

(GAV - Municipal Taxes)Less: Standard Deduction (30% of NAV): ₹24,300

30% of ₹81,000.Less: Interest on Housing Loan: ₹200,000

Entire interest on housing loan is deductible for let-out properties.Less: Pre-construction Interest (1/5th of ₹3,00,000): ₹60,000

Pre-construction interest is distributed equally over five years.Total Deductible Interest: ₹260,000

Total interest deduction includes both current year and pre-construction interest.Income from House Property: ₹(203,300)

This results in a loss of ₹2,03,300, which can be adjusted against other income heads as per tax laws.

Note: For self-occupied properties, the maximum deduction for interest on housing loan under Section 24(b) is ₹2,00,000 per annum. For let-out properties, there's no upper limit on the interest deduction; however, the loss from house property that can be set off against other income heads is restricted to ₹2,00,000 in a financial year. Any remaining loss can be carried forward for up to eight assessment years.

Remember, the maximum loss from the head house property that you can set-off against income from other heads is limited to Rs 2 lakhs. The remaining loss can be carried forward to future years – 8 years in total. However, in these 8 years, it can only be set off from income from house property.

Example of claiming deductions under the following scenario:

Mr. X has 3 house property, 2 are self-occupied and the other one is offered for rent. Interest paid on a home loan of both the self-occupied properties is Rs 3.00 lakhs and interest paid on let out property is Rs. 2.5 lakhs. What all deductions can be claimed by him under house property income?

· Self-occupied properties:

· After the amendment in Budget 2019, Mr. X can claim two property as self-occupied properties with annual value as Nil. Previous to 2019, only one property was allowed to be claimed as self-occupied, the notional rent of the 2nd property was taxable.

· Mr. X can claim a maximum of Rs. 2 lakh of the aggregate deduction (for both the self-occupied properties) against actual home loan interest paid of Rs 3 lakh.

· As the annual value of self-occupied properties is considered nil, income from house property income will become negative after claiming home loan interest. This negative amount can be set off against other income of the current year. Also, the loss amount can be carried forward for the next 8 years which can be set off against future house property income only.

· Rented property:

· In the case of rented property, actual rent received or receivable will be considered as a ‘ Gross annual value’

· Deductions like municipal taxes paid, actual interest on housing loan (no ceiling limit for claiming interest on let out property) will be allowed as deduction. Here, Mr. X can claim actual home loan interest paid of Rs. 2.5 lakh as a deduction for the let out property.

Mr. X can also claim a deduction of up to Rs. 1.5 lakh for principal repayment under section 80C which will be the aggregate of all home loan repayments.