Landmark GST Judgments: A Comprehensive Review for Businesses (Post-April 1, 2023)

Shubham Patel

8/5/202516 min read

I. Navigating India's Evolving GST Landscape

Q1: Why are recent court judgments important for my business under GST?

Since its 2017 launch, India's Goods and Services Tax (GST) system has continuously evolved, and court rulings are vital for clarifying ambiguities and shaping its practical application. These judgments resolve disputes, address legislative gaps, and ensure tax laws adhere to constitutional principles and the rule of law. They serve as authoritative guides, helping businesses navigate compliance and tax administrators enforce laws fairly. Therefore, judicial precedents are crucial for understanding GST's true scope and practical impact, beyond just legislative texts or administrative circulars.

Q2: What is the general approach of courts in recent GST judgments?

Courts consistently aim to strike a balance between safeguarding government revenue and upholding taxpayer rights. They increasingly focus on the substantive aspects of transactions rather than mere procedural technicalities, especially when no revenue loss is demonstrable. This approach provides clarity on complex issues like Input Tax Credit (ITC) on immovable properties and the validity of retrospective amendments. The judiciary also reinforces natural justice principles, emphasizing reasoned orders and proper exercise of discretionary powers by tax authorities.

Q3: How do judicial decisions interact with legislative changes in GST?

Judicial decisions offer definitive interpretations, but they can also prompt legislative responses. For example, the Supreme Court's Safari Retreats ruling directly led to a retrospective amendment in the Finance Act 2025 to nullify its effect. This highlights a risk: a pro-taxpayer ruling, while offering immediate relief, might not be a permanent solution if the government decides to counter it retrospectively. Businesses must therefore constantly re-evaluate their positions based on these dynamic interactions, as the legal landscape is continuously shifting. This interplay means that while judicial rulings provide crucial immediate clarity and relief, they carry the inherent risk of being overturned by subsequent retrospective legislation, necessitating a vigilant approach to compliance.

II. Understanding Input Tax Credit (ITC) Judgments

A. ITC on Immovable Property and "Plant or Machinery"

Q1: Can I claim Input Tax Credit (ITC) on GST paid for building a commercial property like a shopping mall?

Yes, potentially. The Supreme Court in Safari Retreats clarified that if a building functions as a "plant" essential for providing taxable services like renting, you might claim ITC. This depends on a "functionality test" – whether the construction was critical for your taxable activity. The case was sent back to determine if the specific mall qualified, but it opens a pathway for businesses to claim ITC on commercial properties used for taxable supplies, reducing tax costs. This approach acknowledges the economic reality of such structures being integral to the provision of taxable services, helping to mitigate the cascading effect of taxes.

B. ITC Denial Due to Supplier Issues & Retrospective Cancellation

Q2: Can my ITC be denied due to minor invoice errors or if my supplier's registration is cancelled?

Generally, no, if the transaction is genuine and tax is paid. The Delhi High Court in B Braun Medical ruled that ITC shouldn't be denied for minor discrepancies or procedural lapses. Similarly, in

Himalaya Communication, it was held that ITC cannot be denied solely due to retrospective cancellation of a supplier's GSTIN without verifying the transaction's genuineness. Courts prioritize the substance and authenticity of transactions over mere technicalities, protecting bona fide recipients from arbitrary denials. This consistent judicial stance reduces the administrative burden and potential litigation for compliant businesses, implicitly encouraging tax authorities to focus on actual tax evasion rather than procedural policing.

C. Refund of Unutilized ITC

Q3: Can I get a refund of my accumulated ITC if my business closes down?

Yes, the Sikkim High Court in SICPA India allowed a refund claim for unutilized ITC upon business closure. The Court emphasized that ITC, once accrued, is a vested right, and the government cannot retain tax amounts without explicit legal authority. This ruling addresses a legislative gap, ensuring that legitimate credit is not forfeited when operations cease, providing crucial relief to businesses. This determination relies heavily on the fundamental principle that Input Tax Credit constitutes a vested right of the taxpayer, preventing an inequitable outcome where a taxpayer's legitimate credit would otherwise be forfeited.

D. Use of Electronic Credit Ledger (ECL) for Pre-Deposits

Q4: Can I use my Electronic Credit Ledger (ECL) balance to pay the mandatory pre-deposit for filing an appeal?

Yes, the Supreme Court in Yasho Industries upheld that mandatory pre-deposits for appeals can be paid using ITC from your ECL. The Court clarified that the law doesn't restrict payment solely to cash. Since ECL funds are already with the government, using them for pre-deposits doesn't impact revenue collection. This significantly eases the financial burden and streamlines the appellate process for taxpayers, especially Micro, Small, and Medium Enterprises (MSMEs) and export-oriented businesses, aligning with the broader objective of promoting ease of doing business.

E. ITC on Incorrect Tax Heads

Q5: What if I make a genuine mistake and claim ITC under the wrong tax head in my GSTR-3B?

The Kerala High Court in MJBR Marketing ruled that genuine mistakes in classifying ITC under the wrong tax head do not justify penal action if your total ITC balance covers the liability and there's no revenue loss. The court views the Electronic Credit Ledger as a "single wallet with multiple compartments". If the overall balance is sufficient, such technical misclassification should not attract penal provisions, reducing administrative burden. This pragmatic approach acknowledges that internal accounting classifications within the ECL should not override the fundamental principle of credit availability for tax discharge when no actual revenue loss is incurred.

III. Understandings on GST Return Revisions and Timelines

A. Revision of GST Returns

Q1: Can I correct genuine errors in my GST returns even after the deadline, especially if there's no revenue loss?

Yes, the Supreme Court in Aberdare Technologies ruled that correcting bona fide clerical or arithmetical errors in GST returns is a fundamental right, even beyond prescribed deadlines, if no revenue loss occurs. The Court strongly emphasized that "software limitation itself cannot be a good justification" for denying such corrections, as software should facilitate compliance. This judgment elevates procedural flexibility to a constitutional principle, representing a significant pushback against rigid portal designs and statutory timelines. It places a de facto obligation on the government to introduce a formal, structured mechanism for return revisions, akin to the income tax return framework, to reduce litigation and enhance the ease of doing business.

B. Extension of Limitation Periods (Section 168A)

Q2: Can the government extend tax assessment deadlines indefinitely?

No, courts are strictly scrutinizing extensions. The Telangana and Gauhati High Courts (e.g., HCC-SEW-MEIL-AAG JV, Mahabir Tiwari) ruled that a prior "recommendation" from the GST Council is a mandatory prerequisite for extending limitation periods under Section 168A. A subsequent "ratification" or a committee decision is not sufficient. This ensures tax departments cannot indefinitely extend deadlines without strict adherence to statutory conditions, enhancing taxpayer certainty. This judicial insistence on strict adherence to procedural requirements for delegated legislation acts as a vital check on executive power, forcing greater discipline in legislative drafting and implementation of extensions.

Q3: Can a retrospective extension of a deadline revive a tax period that has already expired?

Generally, no. The Allahabad High Court in Anita Traders ruled that a retrospective extension of a statutory time limit cannot apply to periods where the original limitation had already expired. If the original deadline passed before the extension notification was issued, the proceedings are considered time-barred and cannot be revived. This reinforces a fundamental legal principle, acting as a crucial safeguard against indefinite tax liability and arbitrary actions by tax authorities. This strengthens the rule of law within the GST framework, ensuring that executive actions are always within the bounds of properly enacted legislation and do not infringe upon taxpayer rights to finality of assessments.

IV. E-Way Bills and Penalty Rulings: What Businesses Need to Know

A. Technical Errors and Mens Rea

Q1: Will I be penalized for minor typographical errors in my e-way bill?

Not if there's no intent to evade tax. The Allahabad High Court in Gaylord Packers ruled that minor typographical errors, like a single-digit invoice mismatch, don't warrant penalties under Section 129 if there's no intent to evade tax. The Court emphasized that tax authorities must focus on establishing fraudulent intent, not just technical non-compliance. This provides crucial protection for transporters and businesses against arbitrary detention and penalties for unintentional mistakes, compelling enforcement efforts on actual tax evasion. This fosters a more balanced and fair enforcement environment under GST, moving away from a "penalty-first" approach for minor non-compliance.

Q2: What if there's a technical error in the dispatch location on my e-way bill, but no tax evasion?

A mere technical error in dispatch location, without any evidence of tax evasion intent or discrepancy in goods, is not a sufficient ground for imposing penalty. The Allahabad High Court in

M/S SAUMYA quashed such seizure and penalty orders, directing a refund. The Court reiterated that the primary purpose of the e-way bill is traceability and evasion prevention, not punishing bona fide errors, highlighting a practical and pragmatic judicial lens. This consistent emphasis on the necessity of a guilty mind serves as a safeguard against arbitrary penalties, ensuring that penal provisions primarily target deliberate wrongdoing.

B. Mandatory E-Way Bill Compliance

Q3: Is it mandatory to fill both Part A and Part B of the e-way bill, and what happens if I update it after interception?

Yes, carrying a complete e-way bill with both Part A and Part B duly filled is mandatory for goods movement post-April 1, 2018. The Allahabad High Court in

M/S BM COMPUTERS ruled that generating Part B after the vehicle had already been intercepted creates a presumption of intent to evade tax. The Court dismissed arguments of human error, stating such actions don't absolve liability, as technological hurdles have been resolved. This indicates that while minor, bona fide errors might still be excused, fundamental omissions or attempts to rectify issues post-interception will be viewed critically as the e-way bill system has matured.

C. Detention and Release of Goods

Q4: Can my confiscated goods still be released if I pay the fine after the statutory period, but before auction?

Yes, according to the Kerala High Court in Nikhil Ayyappan, goods confiscated under Section 130 can still be released on payment of fine beyond the statutory three-month period, provided they have not yet been auctioned. The Court observed that the law doesn't explicitly prohibit such release and allowing it would not prejudice revenue, especially if goods are still available. Citing principles of equity and fairness, the Court granted another opportunity to pay and secure release. This ruling reflects a judicial inclination towards equity and the preservation of property rights, even when statutory timelines for payment have elapsed.

Q5: Can my vehicle be detained solely based on an e-way bill if there's no actual movement of goods?

No, the Madras High Court in Om Logistics ruled that detaining a vehicle based solely on an e-way bill without any corresponding physical movement of goods is invalid and without jurisdiction. The Court clarified that Section 129 of the CGST Act can only be invoked when goods are actually being transported in contravention of the Act. Since the primary ingredient (movement of goods) was absent, the Court ordered immediate release of the detained vehicle. This ensures that detentions are not arbitrary and that property rights are protected, fostering a more balanced and fair enforcement environment.

Q6: If I pay tax/penalty to release detained goods, does it mean I admit guilt or lose my right to appeal?

No, payment made to secure the release of detained goods cannot be construed as a voluntary admission of liability or a waiver of the right to appeal. The Supreme Court affirmed that every show cause notice must culminate in a final, reasoned adjudication order, even if payment is made during proceedings. This preserves your statutory right of appeal under Section 107, especially since the GST portal lacks a "payment under protest" mechanism. This ensures taxpayers are not deprived of their right to appeal due to practical constraints or procedural ambiguities.

V. Judgments on Constitutional Validity and Legislative Powers

A. Arrest and Summon Powers

Q1: What are my rights if I am arrested or summoned under GST laws?

The Supreme Court in Radhika Agarwal upheld the constitutional validity of arrest and summon powers under GST, but crucially held that the Code of Criminal Procedure (CrPC) applies. This means authorities must inform you of arrest grounds in writing, allow legal representation (within visual range), and produce you before a Magistrate within 24 hours for judicial oversight. Importantly, individuals can also seek anticipatory bail for arrests under the Customs and GST Acts. This landmark ruling meticulously balances the state's legitimate need for effective tax enforcement with the fundamental rights and liberties of individuals, providing vital protection against the misuse of arrest powers.

B. Royalty and State Taxation Powers

Q2: Is royalty on mining considered a tax, and can states levy additional taxes on mineral lands?

The Supreme Court in Mineral Area Development Authority ruled that "royalty" on mining is not a tax; it arises from contractual conditions of the mining lease. However, State Legislatures

do possess the constitutional power to levy taxes on mineral lands and mineral rights. This judgment redefines the fiscal relationship between the Union and States concerning minerals, potentially leading to increased state-level taxation on mineral activities. This case exemplifies the Supreme Court's critical role in resolving complex constitutional ambiguities that have significant economic and inter-governmental implications, showcasing a delicate balancing act between legal principles and economic realities.

C. Classification of Goods and Services

Q3: Who decides how a product is classified for GST purposes, and can the government issue press releases to dictate classification?

Product classification for tax purposes falls exclusively under the jurisdiction of judicial and quasi-judicial adjudicatory authorities, not the executive. The Bombay High Court in

Schulke India quashed a government press release that categorized hand sanitizers as disinfectants, stating the executive cannot dictate classifications. Any adjudication must proceed independently, without being influenced by such executive pronouncements. This firmly upholds the doctrine of separation of powers, preventing the executive from issuing directives that pre-empt or dictate judicial determination of product classification, which is inherently an interpretive function.

Q4: How is flavoured milk classified for GST, and what is its tax rate?

The Supreme Court in Heritage Foods upheld the classification of flavoured milk as "milk" under GST. It confirmed that a 5% tax rate applies under Tariff Heading 0402. This decision provides much-needed clarity and consistency in the classification of a common consumer product within the GST framework, reinforcing consistency in tax treatment.

D. GST Exemption for Regulatory Fees

Q5: Are fees collected by electricity regulatory commissions subject to GST?

No, the Supreme Court in CERC & DERC confirmed that fees collected by electricity regulatory commissions for their regulatory functions are exempt from Goods and Services Tax. The Court explicitly agreed that these regulatory functions are discharged by "quasi-judicial bodies" with the "trappings of a tribunal". Such functions are considered sovereign or public, not "business" activities for GST purposes, thus clarifying their taxability.

VI. Judgments on Supply, Valuation, and Specific Transactions

A. Transfer of Leasehold Rights and Development Rights

Q1: Is GST applicable when I transfer leasehold rights for an industrial plot?

No, the Gujarat High Court in Time Technoplast ruled that transferring leasehold rights for an industrial plot is not a taxable supply under GST. It's considered akin to the sale of land, which is explicitly excluded from GST under Schedule III. The Court noted that such a transaction, involving a complete transfer of rights subject to stamp duty, is treated as an immovable property transfer. This provides clarity that transferring leasehold rights for industrial plots is treated similarly to land sales and is therefore outside the scope of GST, allowing businesses to avoid GST liability on these transfers.

Q2: Is GST leviable on development rights transferred in a joint development agreement (JDA) with a builder?

The Bombay High Court ruled in one specific case that no GST was required if the homeowner merely used the builder's construction service and development rights were not "actually sold/transferred". The transaction must explicitly fall under "transfer of TDR/FSI" as per specific notifications for GST to apply. Businesses must carefully structure their JDA agreements to align with this interpretation and avoid unintended GST liability. This nuanced approach introduces complexity and potential for continued litigation, underscoring the need for clearer legislative guidance or a definitive Supreme Court ruling to provide consistent clarity on various JDA structures.

Q3: Is GST applicable on the sale of an under-construction property by a liquidator on an "as is where is" basis?

No, the Karnataka High Court ruled that GST is not applicable if a liquidator sells an under-construction property "as is where is" without an obligation to provide any construction service to the purchaser. Such a transaction is considered a sale of immovable property, not a taxable construction service. GST on construction applies only if there's a contract for service and consideration received prior to the completion certificate. This provides important guidance for liquidators and purchasers in such scenarios, clarifying the conditions under which such sales are exempt from GST.

B. Secondment of Employees

Q4: Is GST leviable on salaries paid to employees seconded from overseas group companies to my Indian entity?

No, the Karnataka High Court in Alstom Transport India quashed the Integrated GST (IGST) demand on the secondment of employees from overseas group companies. The Court found that a genuine employer-employee relationship existed, which is explicitly excluded from GST under Schedule III of the CGST Act. This judgment provides significant relief to multinational corporations with seconded employees in India, potentially reducing their GST liability. It emphasizes the importance for businesses to carefully structure secondment agreements to clearly reflect a genuine employer-employee relationship.

C. Compensation Cess

Q5: Is Compensation Cess leviable on goods supplied to merchant exporters for export, even if exports are zero-rated?

Yes, Compensation Cess is currently leviable on such supplies due to the absence of a specific exemption notification under the Compensation Cess Act, even though exports are zero-rated for GST/IGST. The Gujarat High Court in

Sopariwala Export acknowledged this causes significant working capital blockage despite being revenue-neutral. The Court referred the matter to the GST Council, urging an exemption to avoid financial strain and promote export competitiveness. This highlights a practical liquidity challenge for manufacturers supplying goods to merchant exporters, putting pressure on the GST Council for policy intervention.

D. Vouchers and Actionable Claims

Q6: When is GST applicable to gift vouchers I issue or accept?

Gift vouchers themselves are generally not liable to GST at the time of issuance, as they are considered "actionable claims" (enforceable debts) and are explicitly excluded from the scope of "supply". GST applies only at the time the voucher is redeemed, and the applicable tax rate depends on the nature of the underlying goods or services actually supplied. However, if a voucher is issued for specified goods or a specified value, GST might apply at issuance. This judgment provides essential clarity for the digital payments and voucher industry, preventing premature taxation of the voucher itself and ensuring GST is levied only on the underlying supply.

VII. Ensuring Procedural Fairness and Natural Justice in GST

A. Opportunity of Hearing and Reasoned Orders

Q1: What are my rights regarding receiving notices and getting a fair hearing in GST proceedings?

Courts consistently uphold natural justice principles. The Madras High Court in Greater Chennai Fine Stamping emphasized the right to a reasonable opportunity to respond to notices and condemned multiple demand orders for the same issue. In

Singh Construction, the Madhya Pradesh High Court ruled that uploading notices only in obscure portal tabs is insufficient communication, requiring re-adjudication with proper hearing. This signifies the judiciary's role as a guardian of due process in the digital tax administration environment, placing a significant burden on tax authorities to ensure digital communication is truly effective and that taxpayers are genuinely aware of proceedings against them.

Q2: Do tax authorities need to provide detailed reasons for their orders, or can they just repeat my submissions?

Tax authorities must provide reasoned and "speaking orders" that demonstrate independent application of mind, not just reproduce your submissions. The Madras High Court in

Tvl Skp Readymix quashed a demand order that lacked substantive analysis or discussion, remanding it for fresh adjudication with a proper hearing. This ensures orders are not mechanical and are legally sustainable, promoting transparency. This reinforces the requirement for tax authorities to issue orders that show independent application of mind, providing taxpayers with a basis to challenge orders that lack proper analysis and reasoning.

B. Provisional Attachment (Section 83)

Q3: Can tax authorities provisionally attach my bank accounts or property without strong reasons?

No, provisional attachment under Section 83 is a drastic and emergency power that must be exercised with utmost caution. The Madras High Court in

Kesar Jewellers ruled it must be supported by tangible material demonstrating a "live link" to potential revenue loss. The order must provide specific reasons, and failure to disclose these reasons constitutes a violation of natural justice, protecting businesses from arbitrary asset freezing. This imposes strict limitations on this power, providing crucial safeguards for businesses against unwarranted and prolonged freezing of assets, which can severely impact operations and liquidity.

Q4: Can my assets be provisionally attached indefinitely or repeatedly without new evidence?

No, provisional attachment ceases after one year from the order date. The Delhi High Court in

Mansi Overseas ruled that a second provisional attachment without any new tangible material demonstrating an attempt to dissipate assets or evade payment is impermissible. Repeated orders without fresh justification are contrary to legislative intent and will be quashed, protecting businesses from indefinite asset freezing. This further restricts the arbitrary use of provisional attachment, ensuring it is not used indefinitely without fresh justification and compelling tax authorities to demonstrate new evidence if they wish to re-invoke Section 83.

C. Blocking of Electronic Credit Ledger (Rule 86A)

Q5: Can tax authorities block my Electronic Credit Ledger (ECL) arbitrarily or for more than my available credit?

No, blocking ECL under Rule 86A is permissible only when backed by material evidence of ineligible or fraudulent ITC. The Supreme Court in

Karuna Rajendra Ringshia affirmed that "negative blocking"—which involves disallowing the debit of more credit than is available or inserting a negative balance—is ultra vires the rule. This protects taxpayers from arbitrary and excessive blocking of ITC without due process, ensuring Rule 86A is a protective measure and not a tool for unlawful recovery. This provides a significant check on the discretionary powers granted to tax authorities, ensuring Rule 86A remains a protective measure against fraudulent ITC utilization, rather than being misused as a tool for tax recovery or arbitrary harassment.

Q6: Do authorities need to give me a hearing or provide clear reasons before blocking my ECL?

Yes, the Orissa High Court ruled that blocking an Electronic Credit Ledger (ECL) without a pre-decisional hearing, a lack of independent and cogent reasons to believe the credit was fraudulently availed, or relying solely on "borrowed satisfaction" from enforcement authorities is procedurally invalid. The Court directed immediate unblocking, emphasizing fundamental principles of natural justice and procedural fairness in tax administration. This reinforces the need for tax authorities to provide a pre-decisional hearing and independent, cogent reasons before blocking an ECL, fostering a more transparent and fair process for taxpayers.

D. Cross-Examination Rights

Q7: Do I have the right to cross-examine third parties whose statements are used against me in a GST adjudication?

Yes, the Gujarat High Court clarified that if statements of third parties form the basis of an adjudication, you must be granted the right to cross-examine them. Failure to allow this can render the adjudication order unsustainable. This ensures you have a fair opportunity to challenge the evidence directly used against you in the adjudicatory phase, promoting transparency and fairness in the final assessment. This draws a crucial distinction in the application of natural justice principles within tax proceedings, preventing tax authorities from relying on unverified or untested third-party statements to impose liabilities or penalties.

VIII. Conclusions on GST Jurisprudence Trends

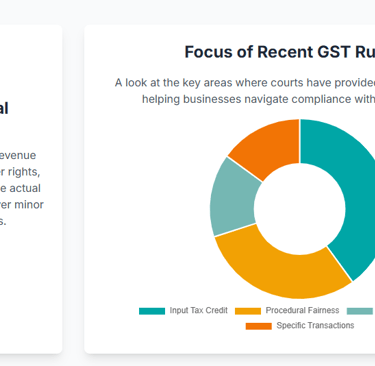

Q1: What are the overarching trends in recent GST judgments?

Recent GST judgments demonstrate a consistent judicial emphasis on balancing government revenue interests with taxpayer rights and procedural safeguards. Courts are increasingly prioritizing the substance of transactions over mere technicalities, particularly where no revenue loss is demonstrable. This approach aims to prevent genuine businesses from being penalized for inadvertent mistakes, promoting ease of doing business and reducing unnecessary litigation. The judiciary also acts as a vital check on executive actions, insisting on strict adherence to statutory prerequisites and constitutional principles.

Q2: How do courts protect taxpayer rights and ensure fair process under GST?

Courts repeatedly underscore the importance of natural justice, mandating reasoned orders, effective communication of notices, and providing adequate opportunities for taxpayers to be heard. Decisions on provisional attachments and blocking of Electronic Credit Ledgers (ECLs) demonstrate a clear intent to curb arbitrary exercise of power, requiring tangible evidence and adherence to strict procedural norms. The application of the Code of Criminal Procedure (CrPC) to GST arrests further reinforces constitutional safeguards, ensuring due process. This signifies the judiciary's role as a guardian of due process in the digital tax administration environment.

Q3: What is the impact of these judgments on GST compliance and administration?

These judgments collectively contribute to a maturation of GST jurisprudence in India, signaling a shift towards a more equitable and predictable tax environment. For businesses, they offer critical guidance for compliance, litigation strategy, and risk mitigation, fostering greater fairness and predictability. For tax authorities, these rulings serve as a reminder of the boundaries of their powers and the imperative of a taxpayer-centric approach to administration, focusing enforcement efforts on actual tax evasion rather than procedural policing.

Q4: Are there any systemic issues highlighted by these rulings that may lead to future changes?

Yes, several rulings bring to light practical challenges and systemic limitations within the GST framework, such as the lack of a "payment under protest" mechanism on the GST portal or liquidity issues with Compensation Cess on exports. While courts provide immediate relief, these decisions also serve as implicit calls for legislative or administrative reforms to address these gaps. This demonstrates the judiciary's active role in identifying and highlighting practical policy issues that hinder business operations, pushing for administrative reforms beyond just legal interpretation. The ongoing dialogue between the legislature, executive, and judiciary will continue to shape the future trajectory of GST in India, with the ultimate goal of fostering a robust and fair indirect tax system.